CBDCs aren’t a threat to Bitcoin, but Bitcoin is a threat to CBDCs

Let’s take a closer look at the myth that central bank issued Central Bank Digital Currencies (CBDCs) will make Bitcoin obsolete.

You might ask: What the hell is a CBDC? In simple terms, it’s a digital currency that is issued directly by central banks. The European Central Bank (ECB) or the Federal Reserve Board (FED) are still evaluating if and how they should introduce their own CBDCs. However, some central banks like the ones in China, Nigeria and Sweden have already started with testing or even the rollout.

Above, you can see the difference between CBDCs (centre) and digital bank deposits (right) we already use. Currently, a retail bank holds bank deposits, and you as a customer deal with them instead of the central bank. Physical banknotes and coins (left) are similar to CBDCs in the sense that you theoretically don’t need a retail bank as an intermediary.

The euro is already digital, but it’s not as centralised as a CBDC

Unlike the digital versions of the Euro and US Dollar we already use, a CBDC would interface directly with the central bank. This means that you wouldn’t need a bank account at a retail bank. Instead, you store your digital money in a digital wallet provided by, e.g. the ECB.

In theory, you have lower counterparty risk as you don’t need a retail bank as an intermediary that could go bankrupt. The ECB calls their CBDC plans “riskless”. CBDCs are in that sense more like cash and less like the digital database entries at your bank.

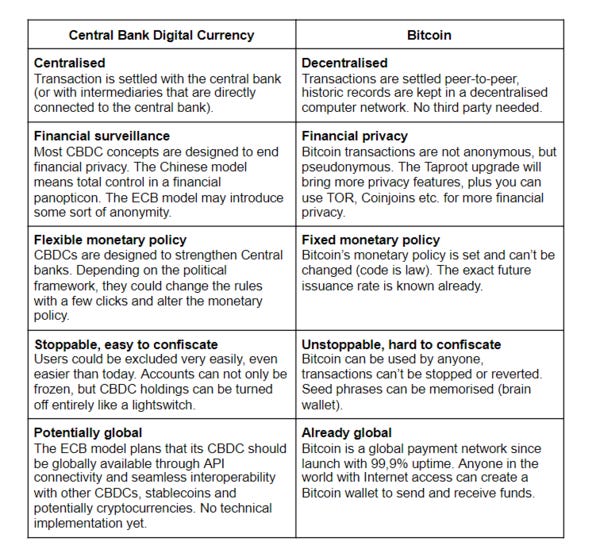

Central banks are trying to maintain control

As cash usage declines, central banks are increasingly under pressure to maintain their monopoly on money. Bitcoin as public money is one factor, but privately issued stablecoins and projects like Facebook’s Libra/Diem could take vast chunks of their monopoly. The primary fear is that as more and more payments happen outside of legacy, regulated payment rails, the harder it gets to implement monetary policy and keep an overview of the already opaque financial system.

The theoretical benefits the proponents of CBDCs like to mention include no transaction and settlement costs, direct access to the population’s wallets to easily distribute stimulus checks or enforce negative interest rates. It’s also a huge upgrade for central banks, as it gives them a lot more power and responsibility than they have today.

CBDCs are digital fiat currencies with more surveillance

Edward Snowden called the concept behind CBDCs a “perversion of cryptocurrency”, a “cryptofascist evil twin” of Bitcoin, placing the state at the centre of every transaction.

And he’s right: With CBDCs, we, the people, are forced to follow the dictates of central banks. So it doesn’t surprise me that politicians and bankers are jealous of what China is doing with their digital Yuan. For example, the president of the German Bundesbank said during a speech in September 2021 that the digital euro is still in its infancy. Still, they are working with Chinese authorities: “The People’s Bank of China took the lead on developing such a digital currency, and we are looking forward to gaining new insights into their projects”.

One key difference to the digital euro we already use is that a CBDC euro would be programmable. This smart money would potentially end money laundering as it would be traceable and identifiable. This means that theoretically, law enforcement could turn money off that was identified as money used by drug dealers, terrorists or political activists.

CBDCs don’t offer any advantage for us, the consumers. It only provides benefits for governments and central banks:

CBDCs makes real-time surveillance of the whole financial system possible

CBDCs allow automated additions (stimulus payments, helicopter money) or withdrawals (negative interest rates, due date for money) at user’s accounts

CBDCs can automatically subtract taxes from user’s accounts

On a larger scale, it makes monetary policy changes effortless to implement and enforce

Bitcoin is the exact opposite of CBDCs

Yes, Bitcoin and CBDCs both allow digital payment. That’s where the similarities end.

CBDCs are in every regard the polar opposite of Bitcoin. CBDCs mean total centralisation; mighty central banks; easy to implement monetary policy changes; complete control of the population by, e.g. adding a date of expiry to money to stimulate consumption (the ECB is openly talking about this in their paper) and the ability not just to ban people from access to bank accounts, but completely turning money off like a light switch.

Bitcoin wasn’t invented only to provide affordable digital payments. It’s a new form of peer-to-peer money that doesn’t require any trusted middleman like a (central) bank or government. Instead, it offers actual ownership and self-sovereignty. Unfortunately, this is something many commentators willingly or unwillingly overlook when they compare Bitcoin and CBDCs.

CBDCs are not a threat to Bitcoin. CBDCs are just fiat currencies on steroids. But, with them around the corner, the value proposition of Bitcoin is getting even more apparent: Digital cash that can’t be controlled, censored, confiscated or stopped by any government. That’s huge.

Satoshi Nakomoto’s famous quote is more relevant than ever:

“The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust.”

Like what you read? Send this newsletter to a friend, subscribe (if you haven’t yet) and follow me on Twitter.

Photo by Etienne Martin on Unsplash.